Healthcare Position Paper

The 7th Congressional District is home to more hospitals, community health centers and other health resources than any other district in the United States. Unfortunately, this district is also home to some of the widest health disparities in the country. The biggest death gap of any U.S. city is found in West Garfield Park. Residents are expected to live on average until 67 years old compared to Loop residents living to 87. Just seven stops on the Green Line Train and a 20-year life expectancy gap.

In Austin, Lawndale, Garfield Park, Humboldt Park and Englewood food and pharmacy deserts are widespread. One of the great crisis in healthcare is inequality and premature deaths based on zip code. The 7th Congressional District, with its healthcare assets, is home to Two Americas of Health and Healthcare Delivery. One system for those with money and another for the poor and uninsured.

Good health and nutrition are our basic rights, not privileges. The federal government must do more to improve the health and nutrition of all Americans. As your Congressman, I will fight to improve access to quality healthcare and nutrition for all. My priorities include:

· Restoring equity and funding for federal health care programs serving vulnerable populations

· Expanding the number of Federally Qualified Community Health Centers

· Increasing minority representation in biomedical workforce

· Ending food deserts

· Lowering the cost of food

· Supporting vaccines, and

· Reducing harm caused by controlled substances, including cannabis

Priority 1 - Restoring equity and funding for federal health care programs serving vulnerable populations

In an unconscionable act of social injustice, the Trump Administration shredded the safety net for vulnerable populations by cutting benefits to fund $4.5 trillion in taxes for the wealthiest Americans. In 2025, the Trump Administration ended subsidies for disadvantaged Americans to afford insurance premiums, cut billions of dollars in funding for health care programs, including minority health care initiatives, and weakened infectious disease control and vaccine programs.

· On December 31, 2025, the U.S. Congress and the President let Affordable Care Act subsidies expire. As a result, more than half a million residents of Illinois may lose access to high quality medical care because they cannot afford the rising costs of insurance premiums for health care.[1] This is unjust.

· Medicaid funding was cut by an estimated $1 trillion over 10 years, which will result in 11.4 million people losing health insurance coverage by the year 2034.[2] This is unjust.

· Supplemental Nutrition Assistance Program (SNAP) was cut by $230 billion, which will result in twenty-two million Americans losing benefits, with monthly family benefits shrinking by up to $146 per month or $1,752 annually.[3] This is unjust.

· Research grants to the National Institute on Minority Health and Health Disparities were cut by $223 million.[4] This is unjust.

As your Congressman, I will fight to restore subsidies for health insurance premiums, Medicaid, SNAP, and other benefits and make the wealthy pay their fair share. Also, I will restore funding to the Office of Minority Health, which is tasked with reducing health disparities, to the NIH for research on various diseases, to the FDA to hire more food inspectors, and to CDC to help prepare us for the next pandemic.

Priority 2 - Expanding the number of Federally Qualified Community Health Centers

In 1965, the federal government set up the Federally Qualified Health Centers (FQHCs) program to provide medical care to underserved populations. The centers provide community residents with access to neighborhood doctors, primary care, behavioral health and dental care. They have a long record of helping to prevent disease and death in underserved communities with limited resources. In addition, they stabilize communities through employment and respond to emerging health care delivery trends, such as tele-medicine. FQHCs receive federal funding and are often run as non-profit organizations. They must meet stringent federal quality standards and must provide services to all patients regardless of ability to pay.

FQHCs are the largest primary care network in the nation. They serve nearly 1 in 10 people, and 1 in 5 Medicaid recipients.[5] In Chicago and surrounding areas, there are 167 FQHCs, ranging from small private homes to large care communities.[6]

FQHCs have been a notable success in providing healthcare and wrap-around services to underserved communities. As your Congressman, I will work to increase the number of FQHCs in the 7th Congressional District and surrounding communities. It is the right thing to do.

Priority 3 – Increasing minority representation in biomedical workforce

In August 2025, the U.S. Department of Health and Human Services ended a long-standing program to help diversify the biomedical workforce.[7] This is unjust. As Congressman, I will work to restore all federal efforts to increase minority representation in the biomedical workforce.

Priority 4 – Eliminating food deserts

The rising tide of wealth has failed to lift all boats. How can Americans flourish when large groups of people are in poverty and ill-fed? Regrettably, communities in Illinois suffer from a lack of available nutritious food. In Cook County, 382 out of 1,319 (28.9%) census tracts qualify as food deserts,[8] which “means a location lacking fresh fruit, vegetables, and other healthful whole foods, in part due to a lack of grocery stores, farmers' markets, or healthy food providers.”[9] This is unacceptable and unjust.

The private grocery industry is not working for these communities because the profit margin is on average 1.6%.[10] Because profit margins are low, private, for-profit companies choose not to sustain a presence in low-income communities in Chicago and Cook County. This is unacceptable because the people who live in these communities suffer from a lack of available, nutritious food.

As your Congressman, I will work with state and local leaders to build a national strategy for ending food deserts and food insecurity. The strategy will include, but is not limited to:

· Providing grants and tax credits for grocery stores supporting underserved areas

· Expanding food banks that provide healthy and nutritious food and ingredients to low-income families

· Increasing funding for SNAP (Supplemental Nutrition Assistance Program)

· Promoting members-supported public grocery stores in the hardest-hit food desert communities

· Working with nutrition related organizations and churches to provide training on healthy eating in communities with the highest levels of obesity, heart disease, high blood pressure and diabetes

· Supporting policies that address social determinants of health, such as housing, food security, environmental justice and employment

Priority 5 – Lowering the cost of food

Recently, the price of food has increased due to inflation. Part of the reason for the rise in inflation is food waste. Waste occurs at all five stages of the food supply chain: production, handling and storage, processing, distribution and marketing and consumption.

Consumers are aware of how to shop for food. Before they go shopping, the consumer will check cupboards and refrigerator for supplies, estimate how much food they need for meals, and make a list before heading to the store. They may overbuy because retailers’ packaging is excessive and sale prices are too good to refuse.

Consumers discard unwanted food due to concerns about contamination and food-borne disease and a need to have the freshest products possible.[11] Some concerns are due to inconsistent definitions of commonly used labels, such as “use by” and “sell by” dates on products. What should consumers do and to whom should they turn for guidance? To address these concerns, the federal government needs to offer clearer food safety guidance for different types of food.

Food retailers and restaurants must reduce food waste and lower costs. Supermarkets and grocery stores can use more resealable packages, offer more variety in package sizes, and offer discount prices for food that are over-ripe or nearing expiration, yet can still be consumed. Also, restaurants can donate excess food, serve smaller portions and provide smaller salad bar plates.

As your Congressman, I will

· Sponsor legislation to require comprehensive safety and waste prevention measures by food type

· Work with food retailers and the restaurant industry to implement cost-effective, best nutrition practices

· Hold hearings in Congress to hold companies accountable for inflated prices and end food delivery monopolies

Priority 6 – Supporting vaccines

The Trump Administration cut or ended billions in funding for 2,500 research grants for vaccine development, chronic diseases, and global health.[12] This is unjust and foolish.

Vaccines save lives and improve the quality of life for all people. Think of the asthmatic child who is allergic to ragweed, grass, molds, dust, and other naturally occurring factors. Those factors can cause severe asthma attacks and can lead to sleep disruptions, higher rates of hospitalization and inability to take part in outdoor activities. In serious cases, a child may need a regime of allergy shots to manage their asthma and lead a more-or-less normal life. This is the benefit of vaccines.

We know vaccines work because scientists can predict that our bodies’ natural defenses will respond in a particular way to the introduction of antigens – and they do, repeatedly. And when we activate our natural defenses, we can beat back deadly and life-restricting viruses and let the asthmatic child enjoy the outdoors, allow parents to manage their households free from the flu, and prevent seniors from experiencing the pain of shingles. Vaccinations are the right thing to do.

It is simple – put science and health above politics. As your Congressman, I will work tirelessly with public health professionals to develop clear, effective, and prompt public health policies and messaging about vaccinations and invest in research that will bring forward new and effective vaccines.

Priority 7 - Reducing harm caused by cannabis

State and local governments have moved too quickly to legalize cannabis for recreational use. They have set up a legal market for cannabis without thinking about the effects of THC on the health of individuals and bystanders.

Recently, scientists published a comprehensive report that “Marijuana users have a 29 percent higher risk for heart attacks and a 20 percent higher stroke risk than their peers who don’t dabble with cannabis.”[13] This is troubling. Why are we allowing profit-seeking cannabis dispensaries to proliferate without mandating health warnings about the risks of cannabis consumption?

Non-smokers have the right to be free from exposure to cannabis smoke in public, including CTA and Metra commuter trains and buses.

The government must protect individuals and communities from substances such as cannabis, steroids, and opioids that can be abused and cause serious harm. As your Congressman, I will work with public health officials to warn consumers about the negative effects of cannabis consumption. Also, I will seek legislation to require mass transit systems that receive federal funds to certify that they are cannabis and cannabis-smoke free.

Conclusion

Good health and nutrition are basic rights, not privileges. I believe the best way to obtain these rights is by putting resources into combatting diseases, providing food security for all, and restricting access to dangerous substances. The priorities I have outlined are a foundation for building communities where access to healthcare is guaranteed, the spread of infectious diseases is stopped in their tracks, where no child or family is undernourished, and dangerous substances are controlled.

Let social justice roll down like water - make healthcare and nutrition a basic right for all Americans.

ENDNOTES

[1] Machi, Sari, Cook County hospitals brace for influx of uninsured patients with Affordable Care Act subsidies expiring, CBS, January 1, 2026. https://www.cbsnews.com/chicago/news/cook-county-hospitals-uninsured-patients-affordable-care-act-subsidies

[2] Galewitz, Phil et al., Five Ways Trump’s Megabill Will Limit Healthcare Access, NPR, July 3, 2025, https://www.npr.org/sections

[3] Konish, Lorie, Trumps’ ‘big beautiful bill’ cuts Food Stamps for millions – the average family may lose $146 per month, report finds, CNBC, July 10, 2025, https://www.nbcchicago.com/news

[4] Palmer, Kathryn, Minority Health Grants Biggest Target of NIH Cuts, May 13, 2025, https://www.insidehighered.com/news/quick-takes/2025/05/13/minority-health-grants-biggest-target-nih-cuts

[5] UnitedHealthcare Community & State Role of Federally Qualified Health Centers in underserved communities, , https://www.uhccommunityandstate.com/content/articles/role-of-federally-qualified-health-centers-in-underserved-commun

[6] See https://carelistings.com/federally-qualified-health-centers/chicago-il

[7] Surina Venkat, Minority health researchers walk tightrope amid NIH funding cuts, The Hill, November 8, 2025

https://thehill.com/policy/healthcare/5592836-trump-administration-nih-funding-cuts

[8] Geocodio, Cook County, IL, Dotsquare LLC, accessed 6/30/25, https://www.geocod.io/

[9] Illinois Department of Public Health, Illinois Food Deserts Annual Report, July 1, 2023 – June 30, 2024, p. 2, https://www.ilga.gov/

[10] FMI, Food Industry Association, Grocery Store Chains Net Profit, accessed 6/30/25, https://www.fmi.org/

[11] Neff, Roni A. et al., Wasted Food: U.S. Consumer’s Reported Awareness, Attitudes and Behaviors, June 10, 2015, https://pmc.ncbi.nlm.nih.gov/

[12] Hwang, Irena et al., The Disappearing Funds, New York Times, June 4, 2025, https://www.nytimes.com/interactive

[13] Physician’s Weekly, Researchers Quantify Magnitude of Cardiovascular Risk Associated with Cannabis, June 18, 2025, https://www.physiciansweekly.com/. See also Weaver, Emily, Marijuana Doubles Your Risk of Dying From Heart Disease—And Edibles May Not be Safer, Best Lie, June 25, 2025, https://bestlifeonline.com/

Nursing Home Care Position Paper

Let Social Justice Roll Down Like Water:

Make Nursing Homes Safe and Welcoming for All

Illinois’ nursing homes are not providing high quality service to our most vulnerable residents. The state’s quality of care scores is near the bottom of state rankings. In 2025, Illinois ranked 47th out of 50, which is a slight improvement from 2019 when the state ranked 49th out of 50. Quality care includes mobility assistance, physical rehabilitation and therapy, nutrition, individualized care plans and prevention of infections, bedsores, and physical injuries, such as bone fractures or dislocation.[i] In some cases, poor care has led to wrongful or premature deaths of seniors who were entrusted to the care of nursing homes. This is unacceptable.

More than 70% of nursing homes are owned and run by for-profit corporations.[ii] Many of them are backed by shell corporations. The shell corporation pays rent to a separate company for the nursing home property and fees to another company that manages the facilities. Under the arrangement, the same owners control each company, make handsome profits, pay lower taxes, and avoid litigation in abuse and neglect cases. This is unacceptable.

Nursing homes will change ownership before they are held accountable for negligence. Litigants who successfully sue nursing homes may not receive compensation due to unclear ownership and corporate financial structures. Furthermore, many nursing homes are under or uninsured, which limits the amount of compensation payable for victims. This is unacceptable.

Regrettably, the Illinois state legislature has failed to create a safe and effective nursing home environment. The legislature has not addressed the greed and indifference of nursing home providers. Also, the legislature has not addressed the racial and ethnic disparities in nursing home care for Illinois’ most vulnerable population. Nursing homes are more segregated by race than any other type of medical facility. These facilities historically are rated poor for quality of service.[iii] This is unacceptable.

As Congressman, I will work to pass legislation that makes neglect of seniors and vulnerable populations in nursing homes a federal crime. Additionally, I will leverage access to federal Medicare and Medicaid funding to ensure those funds are directed toward providing quality care and safety for all seniors and vulnerable populations.

Let social justice roll down like waters. Make nursing homes safe and welcoming for all.

[i] States With High-Quality Nursing Homes, U.S. News and World Report, https://www.usnews.com/news/best-states/rankings/health-care/healthcare-quality/nursing-home-quality

[ii] FastStats - Nursing Home Care, National Center for Health Statistics, Centers for Disease Control, https://www.cdc.gov/nchs/fastats/nursing-home-care.htm

[iii] Addressing Racial and Ethnic Disparities in Nursing Homes, AARP, February 1, 2024, https://ltsschoices.aarp.org/resources-and-practices/addressing-racial-and-ethnic-disparities-nursing-homes

Economic Justice and Consumer Protection Paper

Eliminate Market Manipulation, Unfair Fees, and Price Gouging

Consumers know the price of a product or service is determined by the laws of supply and demand. They recognize that prices go up when the cost of doing business has gone up or demand exceeds supply. When the market changes and prices go up, consumers will modify their spending choices and buy products and services within their means. This system works well when the federal government keeps inflation down, the financial system allows people to keep their money, and the prices of goods and services truly reflect costs plus a reasonable profit.

Regrettably, consumers are losing confidence in the market because they are under assault in several directions:

· The inflation-controlling Federal Reserve System is under attack by the Executive Branch

· Credit card interest rates are exorbitant

· Banks are charging excessive consumer fees

· Businesses are passing the cost of swipe fees down to customers

· Surge pricing is driving up the cost of consumer goods and services

As Congressman, I will take the lead in protecting consumers for financial market manipulation, unfair fees, and surge pricing abuse. I have outlined my plan below for achieving these goals.

1. Protect the Financial System from the Administration’s Market Manipulation

In a prosperous economy, businesses and consumers need a consistent flow of money to function efficiently. In the United States, a complex network of banks, credit unions and other financial institutions keeps money flowing between customer accounts, lends money to businesses and consumers, and invests in communities. The financial system works well because money is backed by the full faith and credit of the federal government. As long as the financial system remains free and independent from politics, Americans will prosper.

Regrettably, the President of the United States is meddling with free and independent financial markets. He is firing members of the Federal Reserve System independent Board of Governors He is pressuring the President of the Federal Reserve to manipulate the U.S. prime rate to advance his political agenda.[i] By interfering in the prime rate-setting process, the President may increase inflation.

Currently, inflation stands at 2.7%. This is well above the annual inflation rate of 2% generally accepted by the Federal Reserve to control inflation, avoid a recession and maintain high employment. By lowering the prime rate, the Administration would pump more money into circulation, causing the price of goods and services to go up further and the inflation rate to jump higher. The price increase would come on top of the rise in consumer prices caused by the Trump Administration’s tariffs. Also, by dictating the prime interest rate, the Administration may push banks to increase customer fees to make up for lost revenue from interest payments. This is bad economic policy.

Let the Federal Reserve Board of Governors do their job freely and independently of politics.

2. Lower Credit Card Interest Rates

About 175 million people in the U.S. have credit cards. High credit card interest rates are causing millions of consumers to get further into debt. As of November 2025, the average credit card interest rate in the United States was 21.39%. Five years ago, in August 2020, the average interest rate was 14.58%.[ii]

Due to increases in interest rates, about 60% of credit card users (105 million users) carry balances forward from month to month.[iii] Also, the number of credit card holders staying in debt for extended periods of time is increasing rapidly. In 2025, about 61% of cardholders with credit card balances (sixty-four million users) were in debt for at least a year, whereas in 2024, 53% of cardholders were in debt for at least a year.[iv]

This is unfair to consumers. They use credit cards primarily to pay for emergencies and unexpected expenses for necessities, including medical bills, as well as car and home repairs. In addition, cash-strapped families are using credit cards to pay for day-to-day expenses such as groceries, childcare and utilities.[v]

As Congressman, I will support legislation to lower interest rates on credit cards to as low as 10% and ensure that consumers continue to have access to credit cards to pay for necessities.

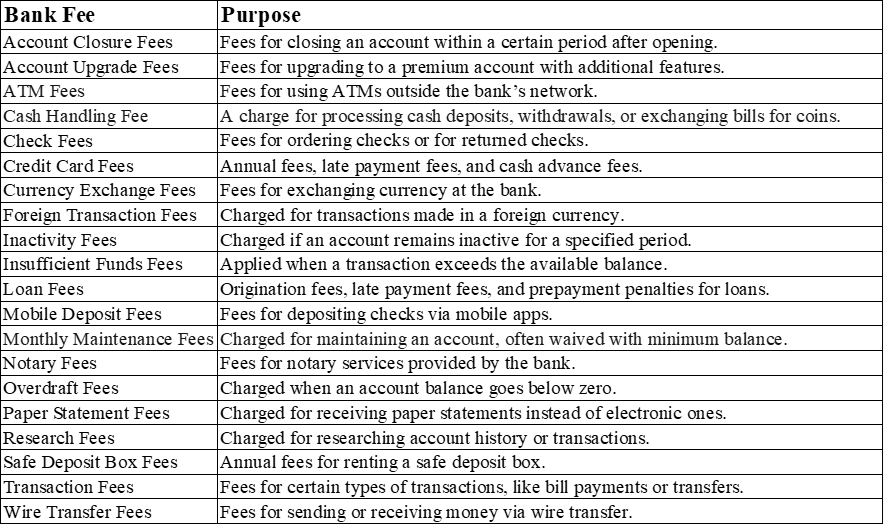

3. Eliminate Unfair Bank Fees

Even without the President’s meddling, consumers are paying excessive fees to generate revenue for banks and financial institutions. A big portion of bank revenue comes from noninterest income, which is fee income collected from investment banking, administration of trust funds, bank sales of loans and leases, underwriting activities and, increasingly, customer service charges such as ATM fees, monthly maintenance fees, and safe deposit box fees.[vi] Between 2001 and 2018, the percentage of bank income from customer service charges nearly doubled. In 2001, service charges represented 14% of non-interest income. By 2018, service charges had grown to 25% of noninterest bank income.[vii]

The primary reason for the increase was the 2008 financial crisis. In the early years of the 21st century, banks made bad decisions that led to the collapse of the financial and housing markets. The federal government had to bail out banks with taxpayer dollars to prevent a complete financial meltdown and run on the banks. We, the consumer, are still paying the price for the banking sector’s failures in the form of higher customer service fees.[viii]

Table 1 shows a selection of fees charged by banks to consumers.

Table 1

Typical Bank Fees Charged to Consumers

I am particularly outraged by fees charged for behaving responsibly. Why should a customer be charged a “prepayment penalty” for paying off a loan early? Why should a customer be charged a “cash handling” fee for using traditional currency, including bills and coins? [ix] Why should customers be charged a “mobile deposit” fee for depositing checks via a mobile app?

This is unfair. It wasn’t meant to be in this way for the average customer, especially for electronic processing of deposits and withdrawals at ATMs. As noted by the Federal Reserve Bank,

“The 1960s saw the advent of automated teller machines (ATMs) and the establishment of local and regional ATM networks. The economics of this expanding network were based on cost reduction (primarily for labor associated with customer checking and savings accounts) rather than on revenue generation as in the credit card model. ATMs offered customers the ability to access their funds after traditional banking center hours by using their ATM cards and PINs.”[x]

We, the customers, loan our money to banks when we make deposits in our checking and savings accounts. In turn, banks pool our money and loan it to individuals and businesses with interest. This is the primary way banks worked before the financial crisis of 2008. Banks should go back to making money in the old-fashioned way: pool our deposits and make loans at sensible interest rates to businesses and families.

As Congressman, I will seek legislation to eliminate unfair bank fees, restrict bank fee expansion, and put a cap on existing bank fee amounts.

4. Eliminate Unfair Swipe Fee Charges for Consumers and Businesses

Banks, credit card companies, and other payment processing networks charge fees that directly impact small businesses and consumers. Known as “swipe fees,” money is paid by businesses to banks and payment processors for every consumer debit or credit card transaction. In turn, many businesses pass the fee costs on to consumers in the form of surcharges or higher prices. [xi]

Why should consumers be penalized for supporting efficient business operations? With a simple swipe or touch of a debit card, credit card, or mobile phone, consumers are helping businesses to deliver thousands of goods and services quickly and effectively at the point-of-sales. Since consumers act rationally and efficiently, merchants can save time because they do not have to manage as many cash transactions. Also, merchant bank accounts are updated in real-time. However, consumers do not receive financial benefit from doing their part. Merchants pass on processing costs to consumers.

Swipe fee rates are mostly set by the dominant credit card networks - Visa, Master Card, American Express and Discover, who collectively set 70% to 90% of the total fee charged for each transaction.[xii] This fee is non-negotiable and must be paid by the merchant. The merchant can negotiate with the payment processor on the markup fee. However, this portion of the total swipe fee is small, usually 0.1% of the transaction value.

The big financial institutions control the marketplace at the expense of consumers and businesses:

· Swipe fee amounts depend on the type of card used, the nature of the business, the volume of transactions and the average value of transactions. Consumers do not control these factors and do not know how much the fees cost. The fees can range from 2.25% to 3.35% of the transaction for credit card transactions. The amount is less for debit card transactions.[xiii]

· Federal law exempts debit card-issuing banks and credit unions worth $10 billion or less from existing swipe fee caps.

· Debit card fees differ based on whether a customer is required to enter a PIN number or sign a sales receipt. The fee is hidden from customers.[xiv]

· Credit card companies make more money from swipe fees when consumers use credit cards, reward cards, premium cards, and business cards. Also, card-issuing banks use swipe fees to fund their cash reward programs. The fee rate is higher for credit cards that offer higher cash rewards program.[xv]

· When a business is in a credit card network, they must accept high reward cards and, therefore, pay higher fees to the network provider. In turn, those higher fees are passed on to all consumers, including consumers who pay by cash or with debit cards. That is very unfair.

· Many businesses cannot afford to be in the electronic payment processing network and are forced to take cash only.

As Congressman, I will sponsor legislation to regulate swipe fees and bring down the cost of goods and services. The legislation will:

· End the PIN vs. signature receipt fee-price difference and charge a uniform fee

· Require credit card companies to charge a uniform swipe fee for reward cards

· Cap the amount credit card companies can charge businesses for swipe fees

· Eliminate the debit card swipe fee exemption for financial institutions valued at $10 billion or less

· Eliminate all swipe fees for debit and credit card purchases of groceries, medical expenses, and public transit cards, such as the Chicago Transit Authority’s VENTRA card

5. End Surge Pricing Abuses

With algorithms and artificial intelligence to guide them, companies can suddenly raise or lower prices at a moment’s notice. Known as “surge pricing,” the practice helps companies increase profit margins at the expense of customers, even when direct and indirect costs have not changed. Companies such as Uber, Door Dash, Amazon, Google, Ticketmaster, and some airlines use surge pricing. Others may follow.[xvi]

Surge pricing can raise the price of any essential consumer product. Take French fries, for example. The direct costs of producing French fries includes the price of land, labor, potato seeds, fertilizer, and pesticides, as well as processing and distributing the final product to stores and restaurants. Along the way, food companies incur indirect costs, such as maintaining company headquarters, advertising, research and development, and financial obligation costs, such as debt service and taxes. These costs are reasonable.

Consumer demand for French fries may increase due to changes in diets and menu offerings. The price will go up until more French fries are produced and supplied to grocery stores and restaurants. This process may take weeks or months to sort itself out.

Surge pricing makes a mockery of supply and demand and hurts consumers. Using a surge pricing model, a fast-food restaurant can charge more for French fries during the peak demand hours of lunch and dinner. That is not fair to consumers, who usually eat lunch and dinner at the same time each day. Consumers work, go to school, and pick up their children at regular times each day because that is the way life is organized. The price of French fries, or any food product, should not surge during normal lunch and dinner hours.

On any given business day, have the direct and indirect costs of producing French fries or any food product changed on an hour-to-hour basis? Did corporate debt payments and taxes skyrocket between the morning coffee break and lunchtime? The answer is no.

Surge pricing is about profit margins. The more a company can charge, the more profit they can make. What better way to earn money than to raise prices and charge more during peak demand hours. This is not the equilibrium price where supply meets demand. This is price gouging.

As Congressman, I will lobby for an investigation into surge pricing. The goal is to determine the extent and reach of surge pricing for essential products and set restrictions as needed.

Conclusion

The federal government can ensure that price setting is fair, equitable and transparent for consumers and the price of a product or service is determined by the laws of supply and demand, only. The plan I have outlined above will help to meet these goals.

Let economic justice roll down like waters. Let’s restore consumer confidence in the market.

ENDNOTES

[i] The U.S. prime rate consists of two parts: the federal funds target rate and basis points. Using data on market conditions, the economic outlook, and prices, the independent Board of Governors of the U.S. Federal Reserve Bank meets regularly to adjust the federal funds target rate. The adjusted rate is added to the rock-bottom base rate of 3.0% (300 basis points) to establish the U.S. prime rate.

[ii] McCann, Adam, Historical Credit Card Interest Rates, WalletHub, November 26, 2025, https://wallethub.com/edu/cc/historical-credit-card-interest-rates/25577

[iii] Dhue, Stephanie, Trump floats 1-year, 10% credit card interest rate cap — what that could mean for your money, CNBC, January 12, 2026 https://www.cnbc.com/2026/01/12/trump-credit-card-interest-rate-cap.html

[iv] Kelton and Staples, op. cit.

[v] Kelton, Katie and Staples, Ana, Bankrate’s 2025 Credit Card Debt Report, Bankrate, January 12, 2026, https://www.bankrate.com/credit-cards/news/credit-card-debt-report/

[vi] Definition of noninterest income: “noninterest income is defined as income generated by banks from sources unrelated to the collection of interest payments.” Haubrich, Joseph & Young, Tristan, Trends in the Noninterest Income of Banks, Federal Reserve Bank of Cleveland, 2019, https://www.clevelandfed.org/publications/economic-commentary/ec-201914-trends-in-the-noninterest-income-of-banks.

[vii] Haubrich, Joseph & Young, Tristan, op. cit. https://www.clevelandfed.org/publications/economic-commentary/ec-201914-trends-in-the-noninterest-income-of-banks.

[viii] “…while banks have not increased their total noninterest income as a share of operating revenues, they have increased one type of noninterest income, namely, income from service charges. The increase in service charges is masked in the data on total noninterest income because other types of noninterest income fell during the same period, specifically, those associated with the financial and housing markets that collapsed during the financial crisis—securitization, trading, and real estate. Finally, we investigate the possible reasons for the changes we observe in banks’ use of the different types of noninterest income. While overall use of noninterest income has decreased, we find evidence that banks have increased their revenues from service charges to make up for interest income lost in the low interest rate environment.” Haubrich, Joseph & Young, Tristan, op. cit., https://www.clevelandfed.org/publications/economic-commentary/ec-201914-trends-in-the-noninterest-income-of-banks.

[ix] Campbell, Travis, Some U.S. Banks Are Now Charging a “Cash Handling” Fee – Even at ATMS, Free Financial Advisor, July 20, 2025, https://www.thefreefinancialadvisor.com/some-u-s-banks-are-now-charging-a-cash-handling-fee-even-at-atms/

[x] Mead, Tim et al., The Role of Interchange Fees on Debit and Credit Card Transactions in the Payments System, Federal Reserve Bank of Richmond, May 2011, https://www.richmondfed.org/publications/research/economic_brief/2011

[xi] What Are Swipe Fees and How Do They Work?, Accounting Insights, August 25, 2025, https://accountinginsights.org/what-are-swipe-fees-and-how-do-they-work/

[xii] Merchant Discount Rate Explained, Merchant Cost Consulting, February 20, 2024, https://merchantcostconsulting.com/lower-credit-card-processing-fees/merchant-discount-rate/

[xiii] Marshall, Madeline, Why Using Your Credit Card Is Getting More Expensive, Wall Street Journal, August 18, 2022, https://www.wsj.com/video/series/wsj-explains/why-using-your-credit-card-is-getting-more-expensive/07DC2C66-80E4-491A-A87F-6C653D089EDD

[xiv] PIN vs. Signature Debit Cards: Similarities, Differences, and Fees, Payment Depot, (accessed 8/26/25) https://paymentdepot.com/blog /signature-debit-cards/

[xv] Marshall, Madeline, op. cit., https://www.wsj.com/video/series/wsj-explains/why-using-your-credit-card-is-getting-more-expensive/07DC2C66-80E4-491A-A87F-6C653D089EDD

[xvi] Salvucci, Jeremy, Surge Pricing: Examples, History and How it Works, The Street, March 21, 2024. https://www.thestreet.com/personal-finance/surge-pricing-definition-examples-how-it-works-uber-lyft-doordash

Make Mental Health Care Services Accessible and Affordable for All

Good mental care is vital for the health and safety of our communities. However, our system of mental health care services is broken. In 2017, only 50 percent of adults experiencing severe psychological distress received any treatment.[i] That was before the pandemic, which led to further spikes in anxiety, depression, and stress for thousands of residents of the 7th Congressional district and elsewhere. We continue to live with the traumatic effects of gun violence, drug and alcohol addictions, and mental health breakdowns in our communities.

Mental health problems are real and serious.[ii]

· Of the 50 million Americans who experience a mental illness, only 45% receive treatment. That means 28 million people are going untreated. This is unacceptable.

· More than 12.1 million adults report serious thoughts of suicide.

· More than 2.7 million youth are experiencing severe major depression.

Local government has mishandled the mental health care needs of underserved communities. In one of the most short-sighted decisions of the last 20 years, the city of Chicago closed six of twelve mental health centers scattered throughout underserved communities. Four of the closed clinics were located on the south side, where poverty, violence, anxiety, and mental illness co-exist. The city took away one of the few public institutions available to help residents grieve collectively, resolve conflicts at home and the workplace before they turn deadly, and be treated for serious mental illness.

And the city’s justification? They could not afford to help us. They said, “Let the private sector and private insurance shoulder the burden.”

What is the result of offloading mental health care responsibility to the private sector? Only people with higher incomes can afford to receive care.

· The prohibitive costs of mental health care are driving patients away from needed care. In fact, “23 percent of adults who report experiencing fourteen or more mentally unhealthy days each month were not able to see a doctor due to costs.[iii] This is unacceptable.

· The number of mental health care deserts nationwide is large. As of June 2022, “over 152 million people in the United States live in a mental health workforce shortage area, and only 28% of the mental health need in shortage areas was being met by mental health providers.”[iv]

· Insurance companies provide lower reimbursement rates for mental health care services than for physical health care services. This is driving practitioners out of the mental health field and forcing patients to use more expensive, out-of-network professionals. “In 2017, 17.2% of behavioral health office visits were to an out of-network provider, compared to 3.2% of primary care providers and 4.3% of medical/surgical specialists.[v]”

· Based on arbitrary and capricious standards, insurers are withdrawing life-supporting coverage during treatment.[vi]

We cannot continue to ignore the heart-wrenching data about the state of mental health of America. As Congressman, I will fight to make mental health care services available and accessible to all Americans.

Boykin Mental Health Care Service Plan and Funding Strategy

Pursuing mental health care reform is one of my top priorities. As Congressman, I will fight for development of community mental health centers, especially in underserved areas in the 7th Congressional district.

· Federally qualified mental health centers will provide treatment services to individuals and families who are low-income or not covered by insurance. Services will be provided on inpatient, outpatient, and emergency bases. Also, consultative, and educational services will be provided through a variety of individual programs that are tailored to the specific needs of our communities.

· I will fight for federal funding for programs that help people with mental illnesses find jobs in the service sector, including administrative, communication, cultural, tourist reception, and other services.

Also, I will fight for legislation to establish uniform insurance coverage practices, based on accepted standards of medical necessity, for mental health care services.

Funding Strategy

Funding for the plan can come from within our community, from private investors and ordinary citizens. We, especially in the Black community, have always taken care of ourselves in the face of obstacles. We have a long tradition of creating and financing our own institutions. I believe that we can dive deeply into that tradition of self-reliance and start the process of restoring community mental health centers through a civic crowdfunding campaign.

Civic crowdfunding is the practice of soliciting and obtaining contributions for public services from a large group of people in the online community.[vii] The funds can be used for discrete projects such as constructing a community mental health center. Using an online app helps to reduce costs, eliminate overhead, and streamline the management of projects through the aggregation of multiple small donations from the community.

When citizens are directly engaged in public finance, they develop a sense of belonging or ownership and help strive to improve quality of life. Municipal crowdfunding platforms help make this possible. The process promotes transparency and ownership because online donations can be processed and tracked efficiently. Furthermore, an audit trail exists for each donation. This will help individuals when they file their federal tax returns and receive a tax deduction on their federal tax returns for making donations to civic projects.

Civic crowdfunding will never provide enough funds. Nor should it because the government has a moral and civic responsibility to make all communities safe and healthy. To start, the federal government should issue a new “social bond” to finance community mental health centers. Recently, Chicago began issuing “social bonds,” which are more affordable than traditional municipal bonds for some investors. In cities that have implemented mini-bond programs, such as Somerville and Cambridge, Massachusetts and Denver, Colorado, bonds are available in minimum denominations of $1,000, as opposed to the traditional $5,000 denomination. Also, the bonds mature in a shorter period. There is no fee to purchase mini bonds if they are purchased online through a recognized underwriting services company.

There are private investors and ordinary citizens who believe that social bonds exist between all communities. Let us give them an opportunity to pool their resources and invest in the mental health of disinvested communities. As Congressman, I will organize a coalition of investors to support the issuance and purchase of federal social bonds. Together, we will rise in health and prosperity.

If civic crowdfunding and social bonds are not sufficient to cover costs, the federal government must provide additional budgetary support for community mental health centers.

As Congressman, I will build a coalition of like-minded colleagues to vote for additional funding to cover costs.

Final Word

Through the inner light of peace and sound mental health, any person can prosper and become a productive member of society. This can be achieved when we provide our children and families with access to high quality mental health services. As Congressman, I will fight to repair our broken system of mental health care services. I will fight for full funding of federally qualified mental health care centers, fund programs that help people with mental illnesses find jobs and require private insurers to adopt uniform standards and definitions of medically necessary services.

Let social justice run down like water. Let’s make our communities prosper by strengthening the mental health and wellbeing of all Americans.

ENDNOTES

[i] Alexa James, Chicago has a mental health crisis; Reopening six clinics is not enough, Chicago Tribune January 22, 2019, https://www.chicagotribune.com/opinion/commentary/ct-perspec-mental-health-clinics-reopen-crisis-city-council-0123-20190122-story.html.

[ii] Mental Health America, The State of Mental Health in America 2023, https://mhanational.org/wp-content/uploads/2024/12/2023-State-of-Mental-Health-in-America-Report.pdf.

[iii] Ibid.

[iv] Ibid.

[v] Ibid.

[vi] Maya Miller & Duaa Eldeib, Her mental health treatment was helping. That’s why insurance cut off her coverage, ProPublica, December 31, 2024, https://www.propublica.org.

[vii] Civic Crowdfunding, The Municipal, June 2, 2015, http://www.themunicipal.com/2015/06/civic-crowdfunding/

Make Parental Leave, Childcare and Early Education Accessible for All

Parents want children of all ages to be healthy, well-adjusted, educated, and productive. For children under age 5 to achieve these goals, parents need access to paid leave as well as childcare and early education (pre-school and pre-K) programs that develop basic social, emotional, physical, and cognitive skills. By committing adequate resources to these efforts, the federal government can give all American children the ability to develop superior math, language and vocabulary skills, enjoy greater self-esteem, and strengthen their ability to work in groups or independently.

Regrettably, these goals are difficult for American families and children to achieve because the federal government has failed to support an affordable, world-class family leave, childcare and early education system. As Congressman, I will fight to create the best possible childcare and early education system for all American families.

Lack of paid parental leave affects family well-being

In the days and months that follow the birth of a child, mothers need time to heal and nurture their babies. The first year of life is critical for a baby’s development, especially for helping them feel confident and safe. Known as “secure attachment,” children who have bonded closely with their parents are usually better at managing emotions and developing strong friendships.[i] For each family, the secure attachment process is unique and requires patience for the relationship to develop naturally.

Regrettably, many families have trouble securing the bond between parent and child in the first year of a newborn’s life due to economic pressures. In most states, the federal Family Medical Leave Act only provides parents with up to 12 weeks of unpaid leave for the birth and care of a newborn child. Just eight states provide paid parental leave for up to 12 weeks. This is an inadequate amount of time and money needed to promote the development of a healthy, well-adjusted child, especially for underserved communities.

Families struggle to obtain and pay for high quality daycare

Even when a parent is ready to go back to work, they face staggering obstacles in finding affordable, high quality childcare services.

· At $13,000 per child, the average cost of daycare in America is straining family budgets.[ii] In Illinois, families are paying 12% of their budget on childcare.[iii]

· For more than 30 years straight, the average cost of daycare and pre-school has gone up faster than the average increase in consumer prices. By April 2024, the costs for daycare and preschool were rising at twice the pace of overall inflation.[iv]

· Parents of children under 5 years of age are quitting work or reducing work hours due to childcare problems. This has led to lower take-home pay up to a staggering $9,026 per year for individual workers, of whom 90% are women.[v]

· Lack of affordable childcare is worse now than before the COVID-19 pandemic of 2020-2022.[vi]

· Many families in Chicago, especially on the west and south sides, live in “childcare deserts,” where childcare options are in short supply.[vii] Furthermore, there are long waitlists for enrolling a child in high quality childcare facilities.

Childcare centers are struggling to stay open

As noted by the respected Center for American Progress, “Even before the COVID-19 pandemic, a typical U.S. childcare business operated with approximately a 1 percent profit margin. The vast majority of childcare providers simply cannot afford to pay workers competitive wages because doing so would require programs to increase tuition beyond what families can pay.”[viii]

Early childhood care and education workers are underpaid and undervalued

Every day in America, about 2.2 million adults, mostly women, are paid to care for and educate more than 9.7 million children between birth and age five in center-based and home-based settings. They are paid poorly. The median wage for early educators is $13.07 per hour, which is much less than the $22.92 in hourly earnings of the U.S. workforce. There is high turnover among early educators and learning centers have significant difficulty in recruiting and retaining staff. [ix]

Uneven access to public pre-school and pre-K education programs

Pre-school and pre-K programs provide many long-term benefits to children. They are more likely to enroll in advanced placement courses, graduate from high school on time, and attend classes.[x] However, fewer than half of 3‐ and 4‐year‐olds in the United States are enrolled in preschool. Most of them go to public schools in states with a strong commitment to providing free early education programs.[xi]

The federal government has failed to meet childcare and early education needs

Federal childcare and early education programs do not meet the needs of American families. At present, the federal government provides a paltry amount in grant funding to the states for childcare and early education grants In 2015, the federal government implemented the Preschool Development Grant Birth through Five program to improve early childhood learning programs. The goals of the programs are to promote choices for early education, monitor and evaluate existing programs, and develop best practices. Under Democratic administrations, the program has expanded to forty-nine states and provided grants to help states. In the current budget cycle, the Trump Administration has called for eliminating funding for the program

In addition, the federal government offers grants to states under the Child Care and Development Block Grant programs. However, funding is limited. The program reaches less than 15% of eligible families.[xii]

Simply put, the federal government is failing to support a world-class childcare and early education system for children under five years old. I am determined to change that. Access to universal paid leave, childcare, pre-school, and pre-K programs is a basic right, not a privilege.

Boykin Five-Point Plan for Paid Leave, Childcare and Early Education

As Congressman, I will fight to support paid leave for the birth of a child, cap childcare costs for working families, increase the supply of high quality childcare centers and programs, increase pay and compensation for early childhood education professionals, and provide funding for universal pre-school and pre-K education for all families.

· Support 12 month paid leave

Only eight states have implemented a paid parental leave policy across the country. The time has come to provide American families with the financial support they need to secure the health and well-being of mothers and babies. As Congressman, I will fight for up to one year of paid leave for every family of a newborn child in America.

· Cap childcare costs for working families

As Congressman, I will fight for the Child Care for Working Families Act, which would cap childcare costs at 7% of income for working families. Also, I will fight for free childcare for Illinois families earning below 85% of the state’s median household income of $85,200.[xiii]

· Increase the supply of high quality childcare centers and programs

We must eliminate childcare deserts in the United States. As Congressman, I will fight to increase grant funding to help defray childcare providers’ costs, including provision of a living wage for staff. Also, I will fight for tax credits for businesses to establish comprehensive childcare services for employees.

· Promote and develop a world class workforce of early childhood education professionals

We must implement a nationwide campaign to encourage the best and brightest among us to provide childcare and early education to young children. As Congressman, I will fight to expand access to scholarships for employees currently working in childcare and early education, as well as fully fund Pell grants for students in college who are pursuing a degree in early childhood education.

· Promote Universal Preschool and Pre-K education

As Congressman, I will fight for federal funding for free, full-day early childhood education for all children aged 3 to 5. Funding would be provided for children with disabilities and children who are learning English. Enrollment in these programs would be voluntary and open to all children without the need for an admission test.

Conclusion

To ensure a better future for Americans, we must respect the value of every newborn child’s life. Right from the beginning of a child’s life, we must establish policies and pay for programs that promote children’s wellbeing and development.

Let social justice roll down like water. Make paid leave, childcare, and early education accessible for all American families and children!

ENDNOTES

[i] Shiffer, Emily, 10 Signs Your Child Has a Secure Attachment—Backed by Psychologists, Parents, December 2, 2025, https://www.parents.com/10-signs-your-child-has-a-secure-attachment-11860518

[ii] Employer-Provided Child Care Credit (45F): Overview, First Five Years Fund, October 29, 2025, https://www.ffyf.org/resources/2024/03/employer-provided-child-care-credit-45f-overview/

[iii] Child Care & Early Learning Help our State Thrive, National Association for the Education of Young Children, 2025, https://www.naeyc.org/sites/default/files/globally-shared/downloads/PDFs/our-work/public-policy-advocacy/state_factsheet_2025_illinois_0.pdf

[iv] Crisis in Childcare and the State of Work in America, KPMG, Mary 28, 2024 https://kpmg.com/us/en/articles/2024/may-2024-childcare-crisis-state-work-america.html

[v] The parental work disruption index: A new measure of the childcare crisis, KPMG, September 30, 2024, https://kpmg.com/us/en/articles/2024/september-2024-the-parental-work-disruption-index.html

[vi] KPMG, September 30, 2024, op. cit.

[vii] Definition: “A childcare desert is any census tract with more than 50 children under age 5 that contains either no childcare providers or so few options that there are more than three times as many children as licensed childcare slots.” Childcare Deserts, Center for American Progress, https://childcaredeserts.org.

[viii] Data Dashboard: An Overview of Child Care and Early Learning in the United States, Center for American Progress, December 14, 2023, https://www.americanprogress.org/article/data-dashboard-an-overview-of-child-care-and-early-learning-in-the-united-states/

[ix] Early Childhood Workforce Index 2024, UC Berkeley, https://cscce.berkeley.edu/workforce-index-2024/executive-summary/key-findings/

[x] Universal pre-K: The long-term benefits that exceed short-term costs, McCourt School of Public Policy, Georgetown University, September 20, 2022, https://mccourt.georgetown.edu/news/universal-pre-k-long-term-benefits-exceed-short-term-costs/

[xi]Preschool Enrollment in the United States: 2005‐2019, U.S. Census Bureau, November 2021 https://www.census.gov/content/dam/Census/library/working-papers/2021/demo/sehsd-wp2021-25.pdf

[xii]New 50 State Analysis Shows Impact of Federal Child Care Program, First Five Years Fund, May 11, 2023, https://www.ffyf.org/resources/2023/05/new-50-state-analysis-shows-impact-of-federal-child-care-program/

[xiii] What is the income of household in Illinois? USA Facts, https://usafacts.org/answers/what-is-the-income-of-a-us-household/state/illinois/